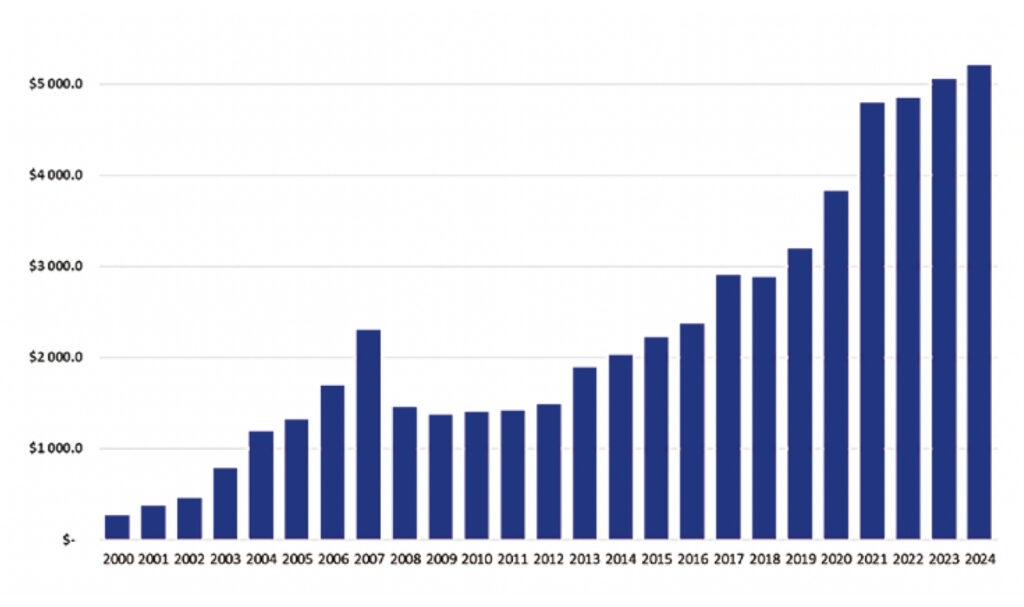

In the ever-changing investment management landscape, diversification remains a cornerstone strategy for both mitigating risks and enhancing returns. Among various alternative strategies, equity long/short hedge funds have gained prominence for their unique risk-return profiles and flexibility. Global adoption of hedge fund investment is evident (see chart 1). The strategy has seen explosive AUM growth over the last decade, from $2 trillion in 2014 to $5.2 trillion at the end of 2024.

Incorporating these funds into an asset allocation mix offers compelling benefits, making them a valuable tool for investors seeking a resilient, capital preservation-focused portfolio. This article explores the key advantages of including equity long/short hedge funds in your investment strategy.

Chart 1: Global hedge AuM $bn

Source: BarclayHedge data

Understanding equity long/short hedge funds

Before diving into the benefits, it’s essential to understand what equity long/short hedge funds are. These funds actively manage a portfolio by taking long positions in undervalued stocks and short positions in overvalued stocks. The goal is to capitalise on security mispricing, generating “alpha”, while also hedging against market volatility.

Unlike traditional long-only equity funds, long/short equity strategies aim to reduce market risk through hedging, focusing instead on stock selection skill. In the main, these funds employ leverage, derivatives, and trading strategies to optimise returns and minimise downside risk participation.

- Enhanced diversification and capital protection

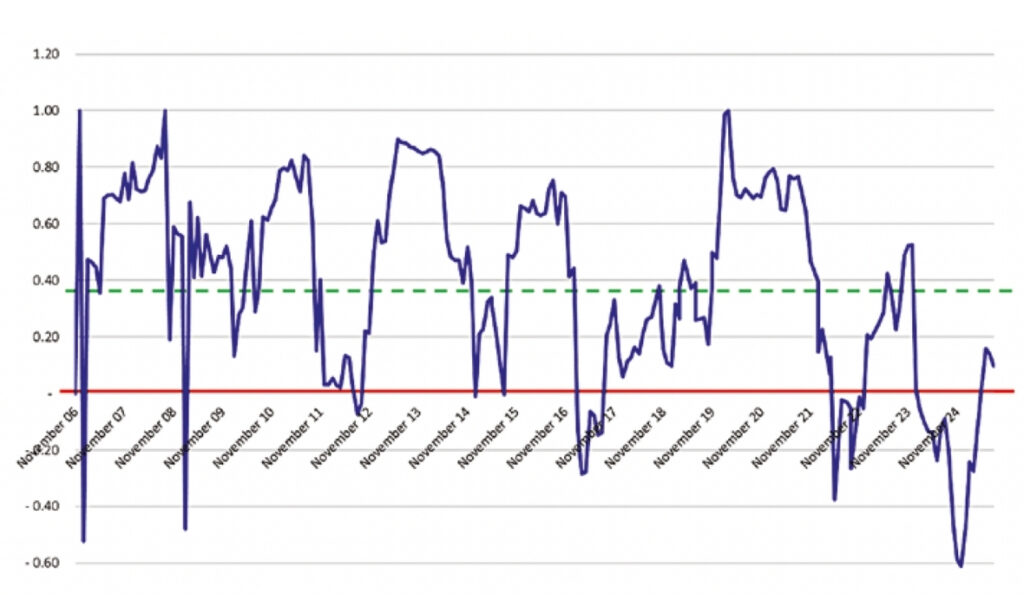

One of the primary advantages of equity long/ short hedge funds is their ability to diversify sources of return and reduce overall portfolio risk. Traditional equity investments are often correlated with market movements, exposing investors to systematic risks. In contrast, long/short strategies can offset market exposure, reduce market beta and create a more resilient portfolio. This is evident in Chart 2, which shows the 12-month rolling correlation of the Visio FR Retail Hedge Fund to the FTSE/JSE All Share Index since November 2006. This has averaged 0.39 for the period.

Chart 2: Visio FR Retail Hedge Fund 12-month rolling correlation vs ALSI

Source: Visio Fund Management, Bloomberg

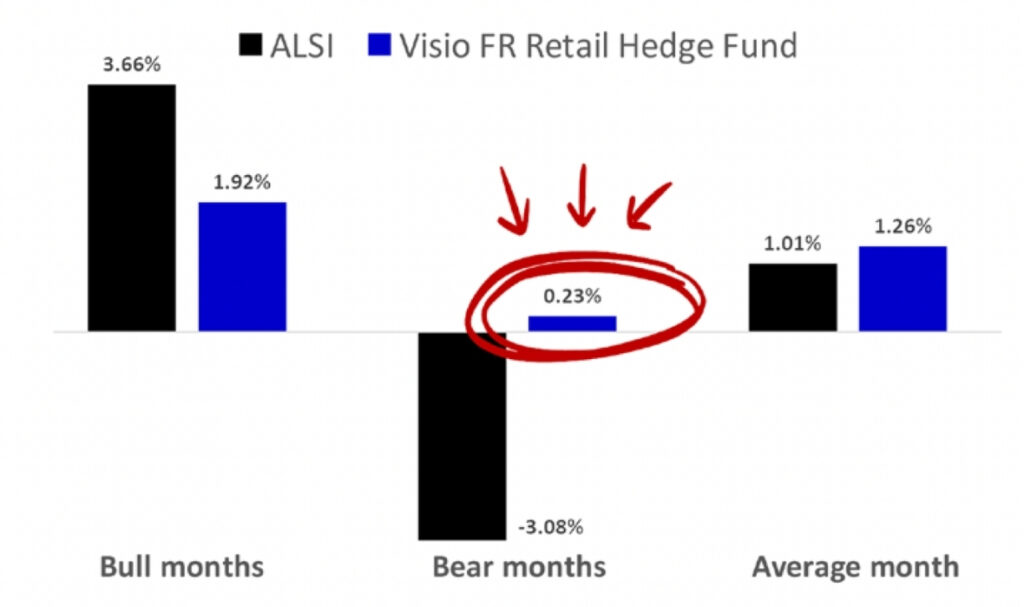

Chart 3: Visio FR Retail Hedge Fund return profile

Source: Visio Fund Management, JSE

By incorporating long and short positions, these hedge funds can diminish the impact of broad market downturns. This diversification benefit is especially valuable during turbulent periods when market correlations tend to increase across traditional asset classes. Including long/short strategies acts as a hedge, helping smooth out and reduce overall portfolio volatility.

Albert Einstein coined compound interest as the Eighth Wonder of the World. He is quoted to have said: “The most powerful force in the Universe is compound interest.” To illustrate this point, chart 3 shows the Visio FR Retail Hedge Fund’s ability to protect capital during volatile markets and to generate absolute returns during bear markets, thereby enabling positive compounding. The cited acceptable equity market downside capture in the industry is for an equity hedge fund to participate in only around 25% of the equity market downside and up to 75% of the equity market upside.

To drive the point home even further, let’s dig deeper into the analytics and look at the upside and downside market capture for the Visio FR Re-tail Hedge Fund monthly. Over the fund’s life of almost 19 years, from November 2006 to August 2025, it has captured half (+1.92%) of the market’s upside during market bull (or up) months, which averaged 3.66% per month. Where Einstein’s positive compounding force comes into effect is the fund’s ability to have generated average returns of 0.23% versus the average ALSI bear month return of -3.08%.

These average absolute returns over both the up and down months for markets result in an average return of 1.26% for the fund, well ahead of the market’s 1.01% average monthly return. For those Warren Buffett fans out there, it heeds to his two rules for investing: Rule #1: Don’t lose money, and Rule #2: Don’t forget Rule #1!

- Alpha generation irrespective of market direction

Equity long/short funds are designed primarily to generate alpha through stock selection and the management of gross and net exposure. Skilled managers identify undervalued and overvalued stocks using in-depth fundamental analysis, proprietary research, quantitative models, and, in Visio’s case, corporate activism.

This ability to outperform markets regardless of broader direction is a clear benefit. During bull markets, the long book positions contribute to upside participation, while short book positions can help protect capital during market selloffs. As a result, equity long/short funds deliver a more stable return profile. This also allows investors to maintain market exposure, or time in the market, reducing the reliance on market timing.

- Dynamic adaptability to market conditions

Given that markets are inherently unpredictable, hedge fund managers’ flexibility to shift allocations between longs and shorts enables dynamic responses to changing conditions. They can position portfolios conservatively during downturns, reining in both aggregate gross and net exposures, or be more aggressive by taking on more market exposure using leverage during bull market cycles.

This active, dynamic nature enables long/short funds to exploit opportunities across different sectors and market environments. It also allows them to mitigate losses in declining markets, providing a form of downside protection that is absent from passive index-type strategies.